26 / 158

26 / 158

26

LISI 2016 FINANCIAL REPORT

The aeronautical division moreover continues the modernization

of its production resources, by investing in the long-term projects

such as the development of the “Optiblind

®

” assembly system, the

implementation of the “robotization” project or again the development

of LISI AEROSPACE Additive Manufacturing. The LISI AEROSPACE

Additive Manufacturing plant was inaugurated in October 2016 and

was certified to produce parts in long production runs for the division’s

major aeronautical customers. Nevertheless, the contribution of this

site will remain negative in 2017.

In 2017, the Manoir Aerospace “Forge 2020” installation project

concerning the plant currently located in Bologne (Haute-Marne) will

enter a concrete work phase.

Other strategic initiatives (Villefranche-de-Rouergue, Dorval [Canada],

Parthenay, Rugby [UK] and Saint-Ouen l’Aumône) will have their full

effect in financial year 2017.

2.3

I

LISI AUTOMOTIVE

Summary presentation of the LISI AUTOMOTIVE activity:

–

–

Organic growth in a still well-focused European market;

–

–

Good dynamic in the mechanical safety components and clipped

solutions activities;

–

–

Fifth consecutive year’s improvement in the operating margin.

Market

The worldwide automotive markets grew by +4.6%* driven by the

Chinese (+12.3%) and European (+6.5%) markets. The American market,

in a consolidation phase, experienced moderate growth of +0.5%.

In Europe, the main area of operations for LISI AUTOMOTIVE, growth

(+6.5%) was driven by the main markets: Italy (+15.8%) and Spain

(+10.9%) stood out from France (+5.1%) and Germany (+4.5%) which

did less well than the market. The UK grew more modestly (+2.3%).

Amongst the Europeanmanufacturers, customers of LISI AUTOMOTIVE,

Daimler (+13.4%), Renault-Dacia (+12.1%) and BMW (10.1%) are the most

dynamic. On the other hand, Volkswagen (+3.3%) and PSA (-0.5%) had

more contrasted performances than in 2015. Orders for new products

taken by the division expressed in annualized sales revenue represents

10.2% of sales revenue, i.e. about €48 million, against about €44 million

in 2015 (9.8% of sales revenue). The growth was particularly remarkable

in the Mechanical safety components Business Group, which expresses

the strategy for gaining market shares in the segment.

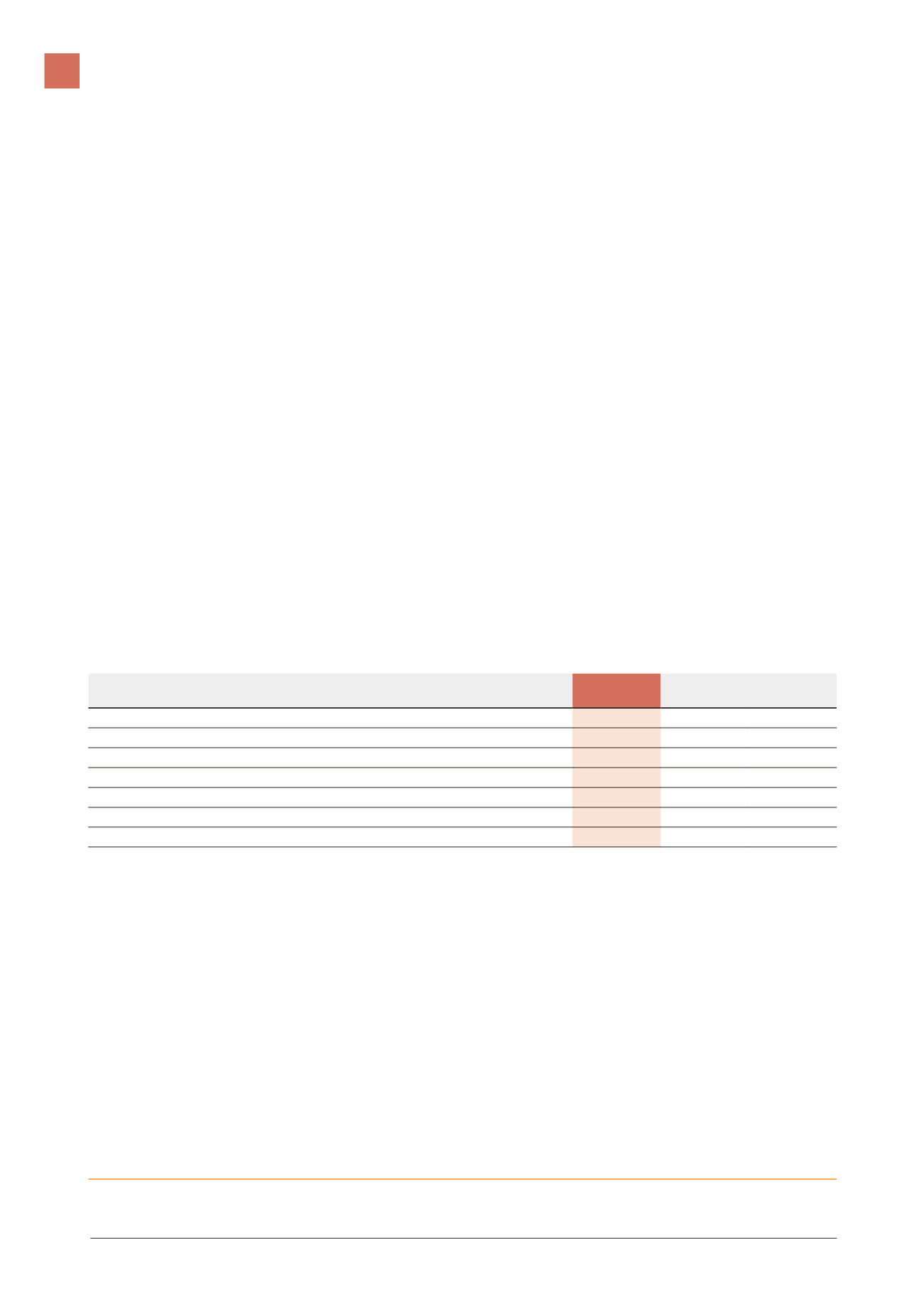

Activity

(in millions of euros)

2016

2015

Changes

Sales revenue

465.3

454.6

+2.3%

Current operating profit (EBIT)

26.3

18.0

+46.2%

Operating cash flow

43.8

32.0

+37.1%

Net CAPEX

(31.9)

(38.3)

(16.7%)

Free Cash Flow

1

7.9

(3.1)

+€11.0M

Registered employees at period end

3,265

3,241

+0.7%

Average full time equivalent headcount

2

3,368

3,330

+1.1%

1

Free Cash Flow: operating cash flow minus net capital expenditure and changes in working capital requirements.

2

Including temporary workers.

After a lackluster start to the year, the division saw a speed up in its

sales in the second half-year (+1.1% at HY1 and +3.8% at HY2). Sales

revenue amounted to 465.3 million, up by +2.3% compared with 2015,

this increase marking the fourth consecutive year’s growth.

This growth, which is less than the volume of the European market,

illustrates the wish of the division to develop selectively in high value-

added products.

Furthermore, the division is continuing its intention to become established

worldwide with encouraging developments particularly in China.

Results

All the “Business Groups” see their performances increasing compared

with last year.

The situation of the French sites in the “Threaded fasteners Business

Group”, and more particularly the Saint-Florent-sur-Cher site, was

markedly improved without, however, reaching the Group average.

Efforts to recover are continuing.

* Source : ACEA Association des Constructeurs Automobiles Européens.

FINANCIAL SITuaTION

2