23 / 158

23 / 158

LISI 2016 FINANCIAL REPORT

23

The policy and organization put in place are based on the international

standard ISO 14001 (international standard governing the environment

management system) as well as on the international standard

OHSAS 18001 (international standard on the health and safety

management system).

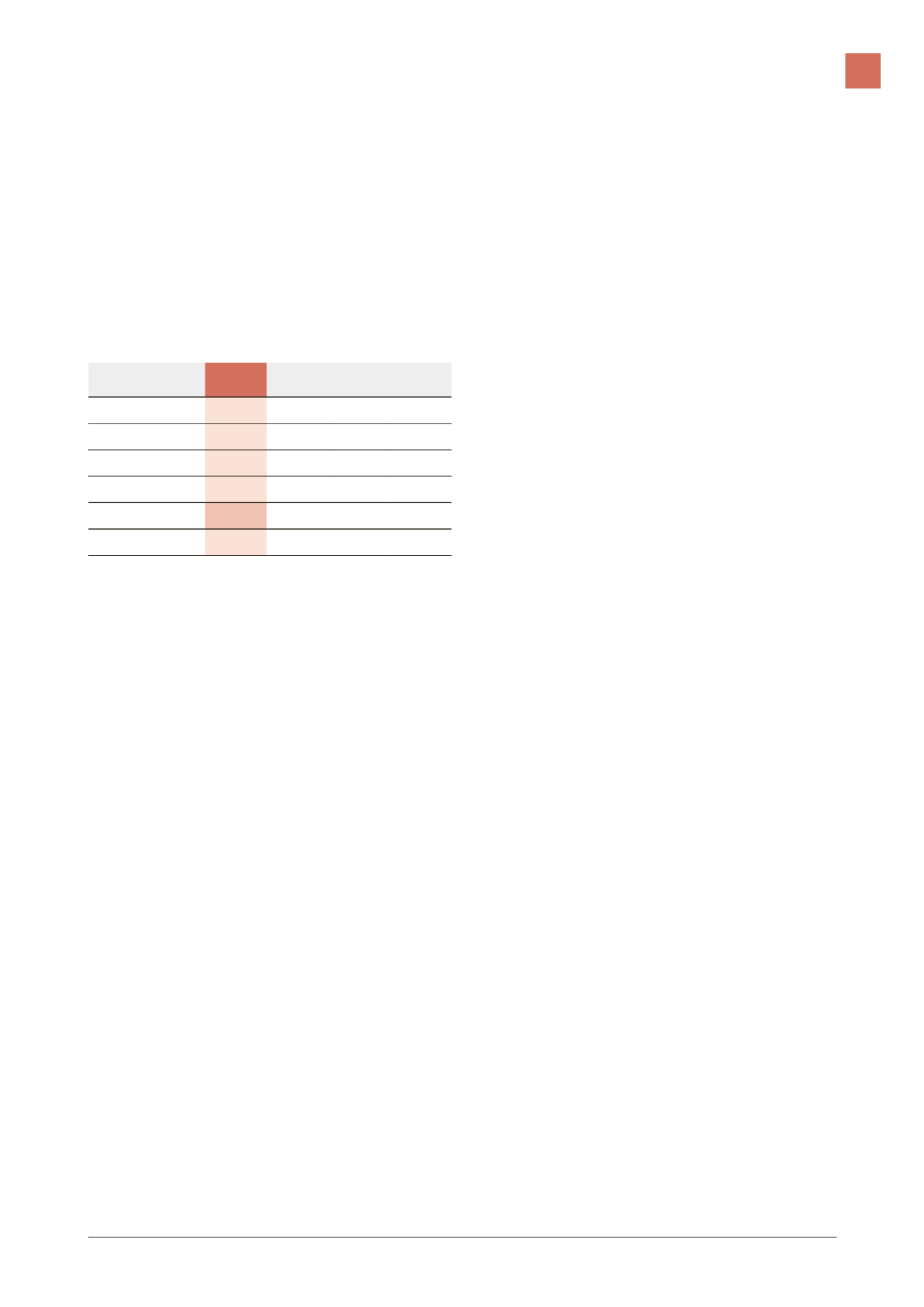

Headcount

As at December 31, 2016, the LISI Group employed 11,587 employees,

an increase of the total workforce of 664 people, which represents a

difference of +6.1% compared to 2015.

Headcount at the end of December

2016

2015

Changes N/N-1

LISI AEROSPACE

7,386

7,087

+299

+4.2%

LISI AUTOMOTIVE

3,265

3,241

+24

+0.7%

LISI MEDICAL

915

573

+342 +59.7%

LISI Holding

21

22

(1)

(4.5%)

GROUP TOTAL

11,587 10,923

+664 +6.1%

Temporary workers

1,156

680

Financial results 2016

2016 is the sixth consecutive growth year for all management

indicators in absolute value.

Gross operating profit (EBITDA) is over €237.1 million, an increase

of +16.2% (+€33 million), and represents 15.1% of sales revenue.

Taking account of the less favorable net effect of the provisions and

reversals than in 2015, the current operating profit (EBIT) grew by

+7.5% (€11.0 million) to €157.5 million at 10% of the sales revenue, the

operating margin is stable compared with the previous financial year.

This resilience is explained by an improvement in the operational

quality of all the Group’s activities which makes it possible to offset the

excess costs generated by the industrialization of the new programs in

the “Structural Components” activity of the LISI AEROSPACE division.

Hence, similarly to the previous year, this level of 10.0% complies with

the objectives of the Group, taking into account its activity mix. The

contribution of the productivity gains from LEAP (LISI Excellence

Achievement Program), the gradual re-orientation of the activities

of the automotive division towards product families with a greater

margin, as well as the effects of the ambitious industrial investment

plan were determining in this performance.

2016 also vouches for the gradual readjustment of the three divisions.

Even if the aerospace division is still the leading contributor to the

current operating profit (ROC at +€122.9 million, i.e. 78% of the Group)

the automotive division shows improved profitability for the fifth

consecutive financial year (at +€26.3 million). The contribution from the

medical division which, as expected, benefits from the consolidation of

LISI MEDICAL Remmele, also improved (at +€9.3 million).

The financial result (+€13.3 million) increased substantially compared

with 2015 (–€16.0 million). The major impacts is summarized by:

–

–

the financial expenses corresponding to the cost in the net debt

benefited from the decrease in the interest rates. They amounted

to –€4.2 million (–€5.0 million in 2015) i.e. an average rate of +1.70%

(+2.06% in 2015);

–

–

the revaluation of the debts and receivables in euros (+€18.3 million

against –€0.1 million in 2015). The value of the debts was

mechanically reduced benefiting from the substantial drop in

sterling, while the value of the receivables, investments and

bank accounts was mechanically increased benefiting from the

substantial rise in the dollar at year end;

–

–

the impact of the unwindings and valuations of the currency

hedging instruments (–€0.7 million against –€9.4 million in 2015);

–

–

the exit from the pension scheme in the United States which had

accounted for –€1.5 million in 2015.

The non-operating costs impacted the non-current result by

–€10.0 million and concern the industrial reorganization of several

major sites (Villefranche-de-Rouergue, Rugby [UK] and Saint-Ouen

l’Aumône) as well as studies on the re-establishment of the Bologne site.

The tax charge, calculated on the basis of the corporation tax as a

percentage of the net income before taxes, reflects an effective average

rate of tax of 33.7%, slightly down compared with 2015 (34.3%).

At €107.0 million, the net earnings thus clearly exceeded those of

2015 (€81.8 million), greatly improved by the financial earnings for the

financial year.

The shares substantially increased to €2.02 (€1.55 in 2015).

Based upon the results, the Group will seek the approval of the

Shareholders’ General Meeting to set the dividend at €0.45 per share

for the 2016 financial year.

The financial structure is still solid after three years of significant

investments

In a context where the levels of activity are strongly increasing, the

reduction in the levels of inventories (–6 days expressed in days

of sales revenue) and the further decrease in late payments by

customers enabled the consolidated working capital requirement to

be maintained at 76 days in 2016.

Following on from previous years, LISI maintained a steady pace

of capital expenditures that reached a historically high level of

€119.6 million. In 2016, they were mainly devoted to equipment specific

to new products and to the extension and re-establishment of several

major sites (Villefranche-de-Rouergue, Rugby [UK] and Saint-Ouen

l’Aumône). With €195.8 million of operating cash flow (+€41.6 million,

12.5% of consolidated sales revenue, to be compared with 10.6% in

2015), the Group was easily able to cover these, while at the same

time still generating a positive

Free Cash Flow

of €73.5 million, in the

three divisions.

FINANCIAL SITuaTION

2