46 / 158

46 / 158

46

LISI 2016 FINANCIAL REPORT

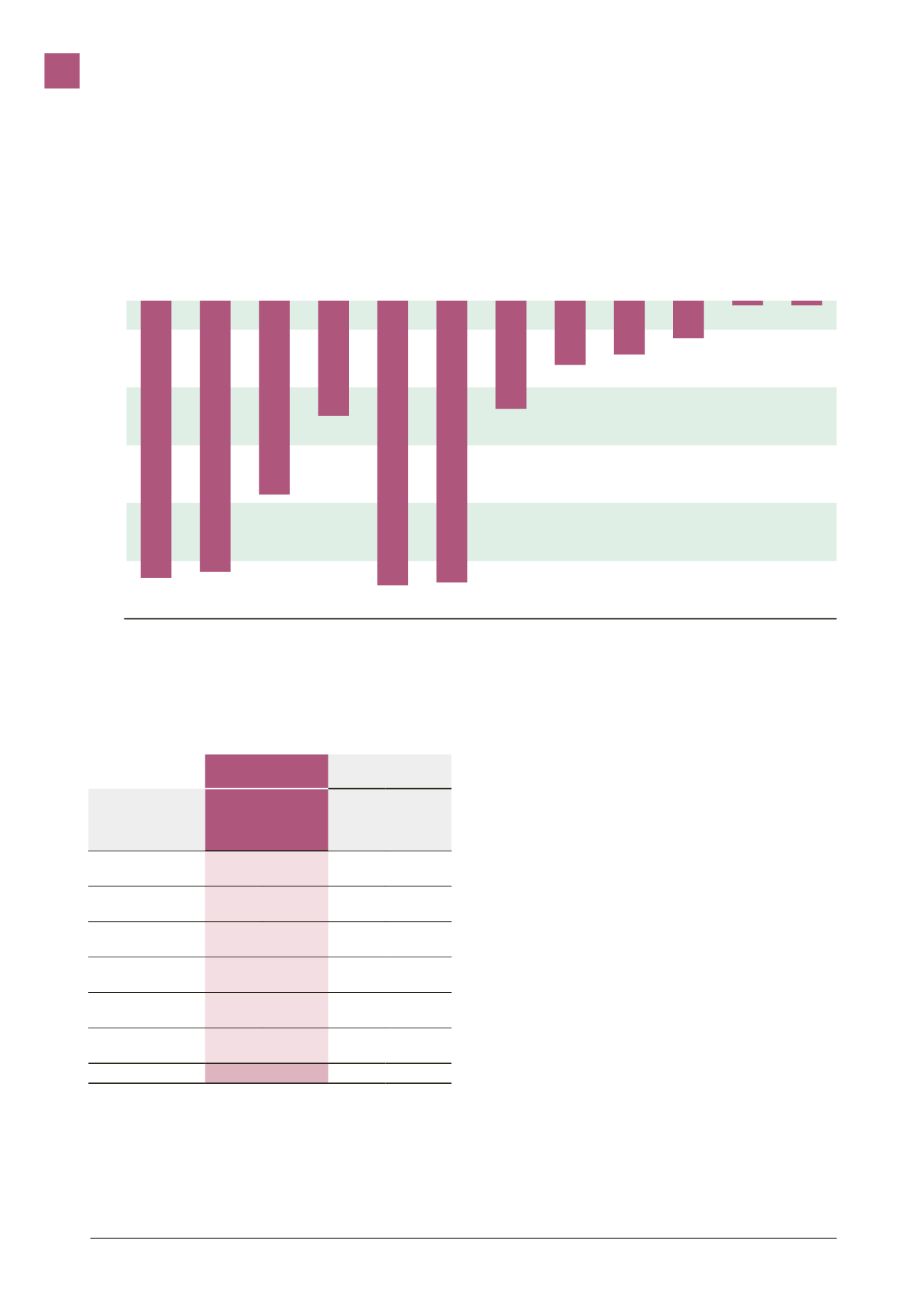

The graph below shows the Group’s financial leeway over ten years,

giving a total borrowing amount of €295 million. The difference with

the current and non-current borrowings shown above (€360 million vs.

€295 million) is primarily due to current banking facilities, employee

profit-sharing and leasing liabilities that are not included in the graph

below:

In €’000

Debt amortization profile at 12/31/2016

–55

–50

–45

–40

–35

–30

–25

–20

–15

–10

-5

0

2028

2027

2026

2025

2024

2023

2022

2021

2020

2019

2018

2017

–0.8

–0.8

–6.5

–9.3

–11.1

–18.7

–48.7

–49.2

–19.9

–33.5

–46.9

–47.9

2.4.3

I

Market risk

The main risks covered by the Group’s financial instruments are the

foreign currency risk and the interest rate risk. The fair value as at

December 31, 2016 of the derivatives used in the management of

market risks is detailed below:

12/31/2016

12/31/2015

(in €’000)

On the

assets

side

On the

liabilities

side

On the

assets

side

On the

liabilities

side

Interest rate risk

management

Variable rate

payers swaps

2,056

1,893

Currency risk

management

Foreign exchange

derivatives

23,281 2,151

14,052

Raw materials

management risk

Raw materials

derivatives

145

TOTAL

0 25,482 2,151 15,945

Market risk is the risk of variation in market prices, such as interest rates,

affecting the Group result or the value of financial instruments held.

Managing market risk involves controlling market risk and maintaining

it within acceptable limits, whilst optimizing the profitability risk ratio.

The Group buys and sells derivatives and supports financial liabilities

in order to manage market risk.

Hedging and market operations on interest rates, exchange rates or

securities using futures instruments are recorded in accordance with

the provisions of CRBF rules nos. 88-02 and 90-15. Commitments

relating to these transactions are posted to off-balance sheet

accounts for the nominal value of the contracts. As at December 31,

2016, the sum of these commitments represented the volume of

transactions that remained unsettled at year-end.

The accounting principles applied vary according to the nature of the

instruments and the operator’s initial intentions.

The commitments are detailed in paragraph 2.8.4.1 of chapter 3 of

this Annual Report.

2.4.3.1 Interest rate risk

The Group’s main exposure in terms of interest rate risk arises from the

exposure of its financial assets and liabilities at variable rates to variations

in interest rates, which could have an impact on these cash flows.

Within the framework of its overall policy, the Group partly converts its

initially variable rate liabilities into fixed rate liabilities, using financial

instruments such as interest rate swaps.

These hedging instruments are negotiated on OTC markets with

banking counterparts, in a centralized manner by the Group’s Financial

Department. They are not considered by the Group to be hedging

instruments and are recorded at fair value to the income statement.

CONSOLIDATED FINANCIAL STATEMENTS

3