24 / 168

24 / 168

advance that will consolidate its differentiation in a sustainable manner

in very strongmarkets over time.

2.2

I

LISI AEROSPACE

Summary presentation of the LISI AEROSPACE activity:

■■

sales revenueswere above €1 billion for the first time, but with a strong

disparity inorganicgrowthbetweenthefirsthalf(+7.4%)andthesecond

(-1.1%);

■■

improvement of all management indicators over the year, with a sharp

contrast between the first and second half of the year affected by the

temporary adjustment of Airbus inventories and the adverse effect

related to the decline of the dollar against the euro;

■■

positive free cash flow after a strong increase in investment plans

(+11.0%);

■■

a difficult start to 2018 in line with the second half of 2017.

Market

Visibility in the commercial aircraft segment remained very solid in

an environment in which global air traffic was experiencing sustained

annual growth (+7.7%* in 2017). The other market segments served by

LISI AEROSPACE, including military, business aircraft and regional

aircraft still show no perceptible signs of recovery. The helicopter

market seems to be slowly recovering.

Although Airbus delivered fewer aircraft than Boeing (718 aircraft

delivered versus 763 for Boeing), it remains the leader in the number

of net orders (1,109 versus 912 at Boeing). The backlog for both aircraft

manufacturers is over 13,000 airplanes. As expected, the impact of

increases in delivery rates of single-aisles (from 1,035 to 1,087) and of the

A350, which accelerated from49 to 78 deliveries, will continue in 2018.

For its part, Safran continues to benefit fromof the steep rise in delivery

rates of theLEAPengine (more than450engines delivered in 2017, nearly

6 times more than in 2016) with a backlog of more than 14,000 engines.

This growth rate is expected to almost triple in 2018.

* Source: IATA.

Activity

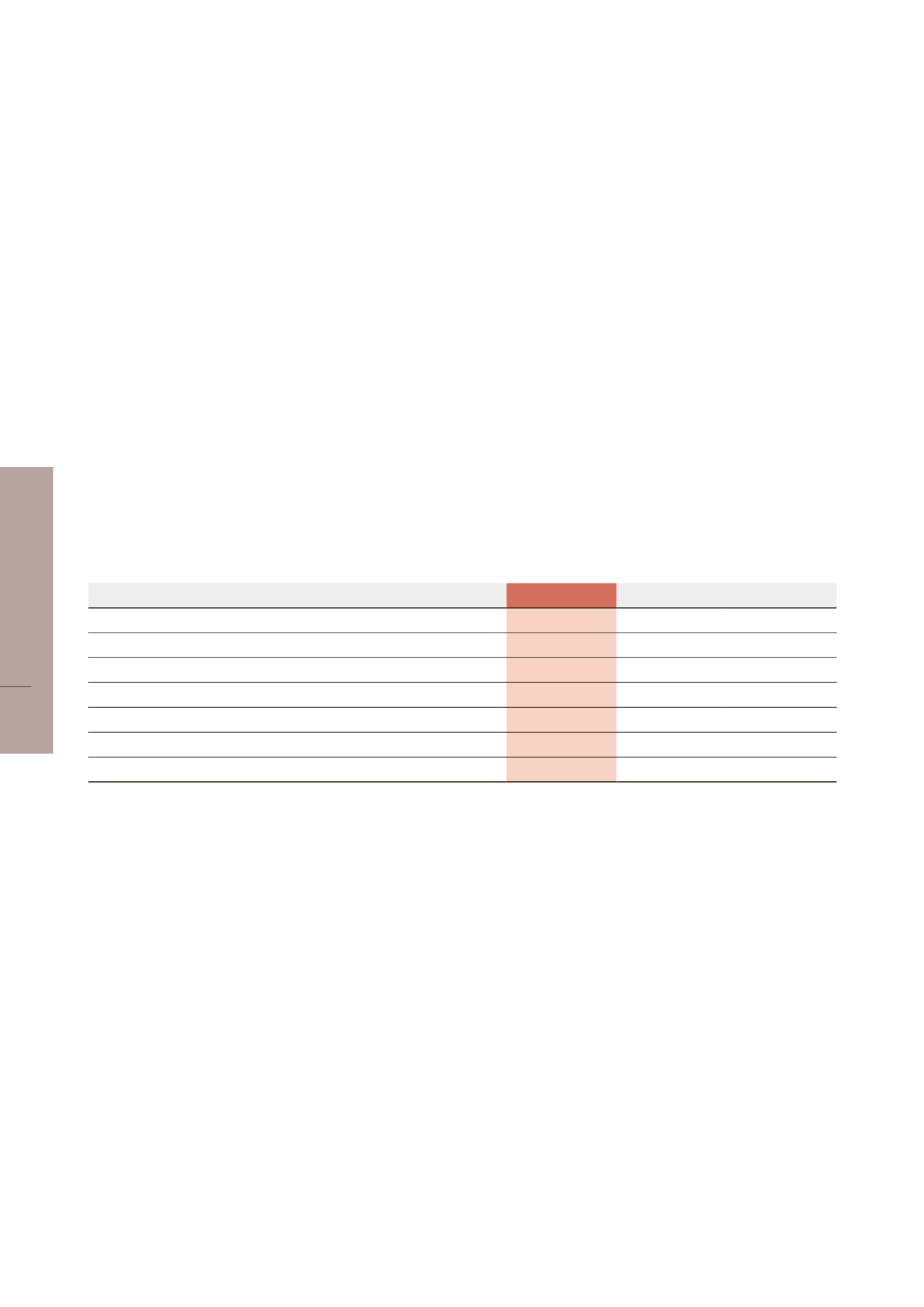

In millions of euros

2017

2016

Changes

Sales revenue

1,000.9

987.2

+ 1.4%

Current operating profit (EBIT)

128.1

122.9

+ 4.2%

Operating cash flow

129.9

127.1

+ 2.2%

Net CAPEX

- 91.4

- 82.4

+ 11.0%

Free Cash Flow

1

61.6

32.3

€+29.3 million

Registered employees at period end

7,251

7,386

- 1.8%

Average full time equivalent headcount

2

8,223

8,011

+ 2.6%

1

Free Cash Flow: operating cash flowminus net capital expenditure and changes in working capital requirements.

2

Including temporary workers.

At €1,001 million, sales revenues reached a historical level, up 1.4%

compared to 2016 and 3.3% at constant scope and exchange rates.

The “Fasteners Europe” activity was negatively impacted by the Airbus

destocking in the second half of the year. As a result, deliveries were

down 7.8% in the second half of the year after a very dynamic first part of

the year (+13.7% in H1). Airbus adjusted onsite inventory levels after the

industrialization and launch phase of the A350 and A320neo (phase-in).

Theaccelerateddepreciationofthedollaragainsttheeuroalso impacted

the division’s performance negatively. In the United States, “Fasteners”

activity picked up steam at Boeing, while the active repositioning of

LISI AEROSPACE with the distribution sector was hampered by low

activity levels for business and regional aircraft. On the other hand,

the “Structural Components” activity had strong sales revenue growth

comparedto2016withthecontinuedramp-upofnewprograms,including

the LEAP engine.

Results

Current operating profit totaled €128.1 million, up €5.2million from2016.

At +12.8%, the operatingmargin increased by 0.4 points compared to the

previous financial year.

The production sites for the “Fasteners” activity benefited from a

favorablevolumeeffectinthefirsthalfoftheyear.Theproperadjustment

of production costs in the second half of the year limited the negative

impact of lower volumes for Airbus on operating profit. In addition, the

improvement intheoperationalsituationofthe“StructuralComponents”

activity is underway, and the additional costs generated by the industrial

difficulties in the steep acceleration phase for new programs were

reduced by half over the year according to the road map that was

established.

24

LISI 2017 FINANCIAL REPORT

FINANCIAL SITUATION

2