LISI FINANCIALREPORT2013 I

41

CONSOLIDATEDFINANCIALSTATEMENTS

3

TheGroupbuys and sellsderivatives and supports financial liabilities in

ordertomanagemarketrisk.

Hedging and market operations on interest rates, exchange rates or

securities using futures instruments are recorded in accordance with

theprovisionsofCRBF rulesnos.88-02and90-15.Commitments relating

to these transactions are posted to off-balance sheet accounts for the

nominalvalueofthecontracts.AsatDecember31,2013, thesumofthese

commitments represented the volume of transactions that remained

unsettledatyear-end.

The accounting principles applied vary according to the nature of the

instrumentsandtheoperator’s initial intentions.

Thecommitmentsaredetailed inparagraph2.7.4.1ofthisannual report.

Interest rate risk

TheGroup’sprincipalexposureintermsofinterestrateriskarisesfromthe

exposureof itsfinancialassetsand liabilitiesatvariableratestovariations

in interestrates,whichcouldhavean impactonthesecash flows.

Within the frameworkof itsoverall policy, theGrouppartly converts its

initially variable rate liabilities into fixed rate liabilities, using financial

instrumentssuchas interestrateswapsand interestrateoptions.

These hedging instruments are negotiated on OTC markets with

banking counterparts, in a centralizedmanner by theGroup's Financial

Department. They are not considered by the Group to be hedging

instrumentsandarerecordedat fairvaluetothe incomestatement.

In2013, theGroupdidnotputanynewhedges inplaceand theamount

of its unexpired instruments at December 31, 2013 covered a nominal

amount of €56.5m. The features of these instruments are presented in

note2.7.4 "Commitments".

As at December 31

st

, theGroup’s net variable rate positionbroke down

as follows:

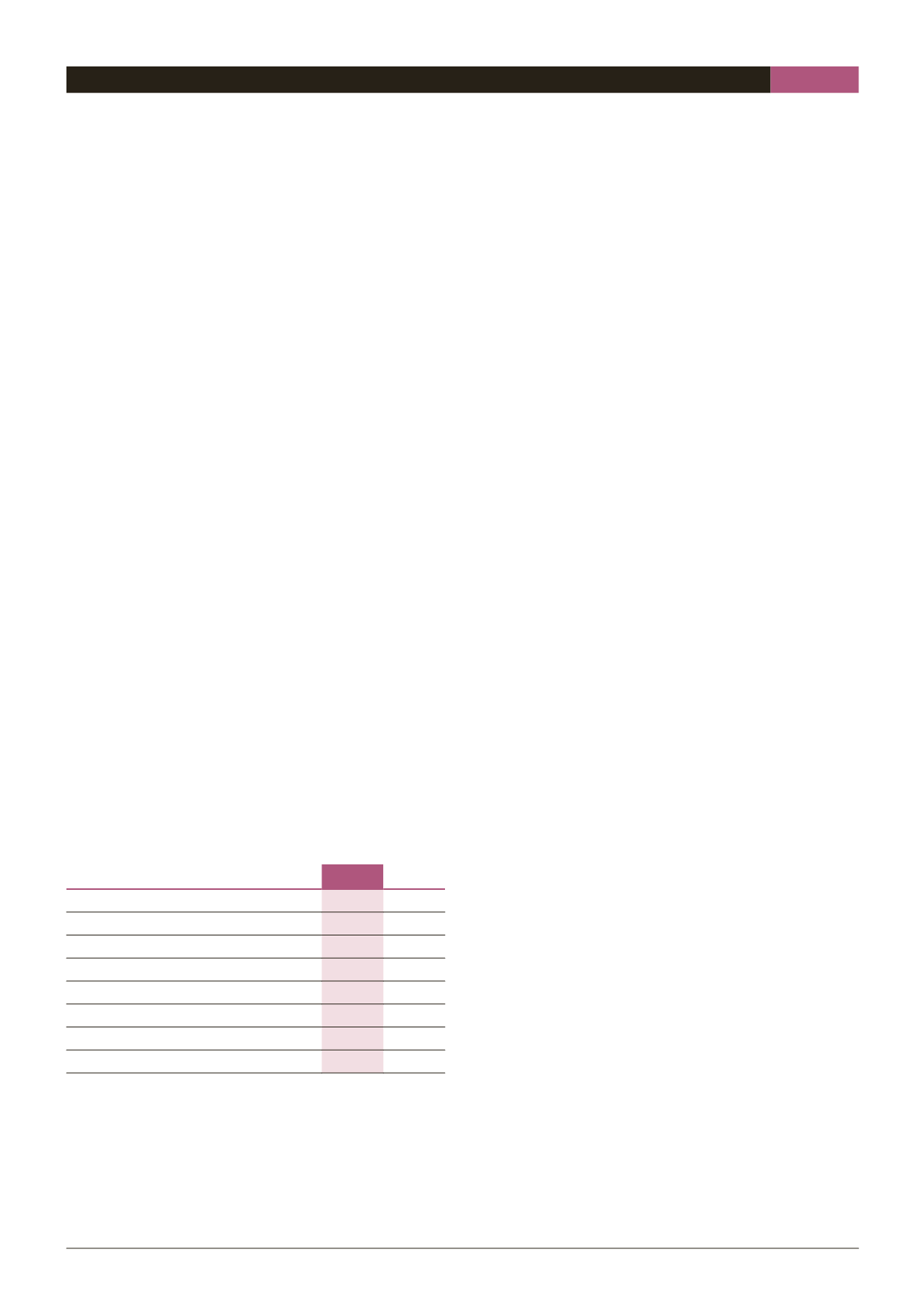

(In€'000)

12/31/13

12/31/12

Loans–variable rates

71,542 138,900

Short-termbanking facilities

8,224 10,892

Other currentandnon-current financial assets

(35,892)

Cashandcashequivalents

(78,600)

(30,625)

Netpositionprior tomanagement

1,166 83,275

Interest rateswap

56,491 75,353

Hedging

56,491 75,353

Netpositionaftermanagement

(55,325)

7,922

Theapproachtakenconsisted intaking intoaccountasacalculationbasis

forthesensitivitytoratesthenet, lendingandborrowingpositions.

As at December 31, 2013, the impact of the nonhedgedportion of 100

basepointsofvariableratechangestoodat+/-€0.6million.

Commoditiesprice fluctuation risk

This issue isdealtwith inChapters5§4.6.1.

Currency risk

Overall, theGroup issubjecttotypesof foreignexchangerisk:

n

Outside the EUR and USD zones, it has production facilities in a

dozen countries, inwhich themajority of the sales of its subsidiaries

are denominated in EUR or in USD, whereas their costs aremainly

denominated in local currency,which is theGBP, CAD, TRY, CZKand,

to a lesser extent, theMAD, CNY, INR andPLN, giving rise to a cash

requirement in local currencies. A strengthening of these currencies

wouldaffectthebusinessperformanceofthegroup;

n

TheUSDconstitutes thesecond invoicingcurrencyof theGroup, after

the EUR, mainly in the LISI AEROSPACE Division. Invoicing in other

currencies isnotsignificantattheGroupscale.AweakeningoftheUSD

wouldaffectthebusinessperformanceoftheGroup.

Inordertoprotect itsresults,theGroup is implementingahedgingpolicy

aimed at reducing the factors of uncertainty affecting its operational

profitabilityandat giving it the timenecessary toadapt its costs toany

unfavorablemonetaryenvironment.

Hedgingof the foreignexchangeon risk local currencies

TheGrouphas verygood visibilityover its local currency requirements.

Also, it hedging policy is based on themanagement of a portfolio of

financial instruments enabling it not to descend below a parity floor,

whilstenabling itwhereapplicabletobenefitfromapartial improvement

in the underlying parities, without however putting at risk the original

floor.Thehedginghorizon is12-24months.

HedgingofUSDcurrency risk

As indicated above, the generation of USD arises mainly from the

Group's LISI AEROSPACE Division, which benefits from long-term

contracts providing for invoicing in this currency. The hedging policy

is based on themanagement of a portfolio of financial instruments ,

enabling it toobtainanoptimizedhedging rateby reference tonormal

market terms. Thehedginghorizonmayextendoverup to8years. This

strategy enabled theGroup, in 2013, to sell a total amount of USD 10.4

million atanaverageratecloseto1.18.